Aina Haina Flood Zone Buying: Tsunami & FEMA Guide

March 24, 2026

March 24, 2026

You can fall in love with ʻĀina Haina’s ocean views and still buy with clear eyes about flood and tsunami risk. If you are eyeing a home makai near Maunalua Bay or upslope mauka toward the ridge, understanding the two different map systems that guide safety and insurance will save you time, money, and stress. In this guide, you’ll learn how to read both tsunami and FEMA flood maps, what that means for lending and insurance, and which documents to request before you commit. Let’s dive in.

Hawaii’s tsunami maps are built for evacuation planning. The state provides interactive maps and downloadable neighborhood insets that show evacuation zones along the shoreline and identify extreme tsunami areas. Use these maps to plan where you would go on foot and how your family would evacuate if needed. Start with the state’s official tsunami resources on the Hawaii Emergency Management Agency site.

FEMA Flood Insurance Rate Maps (FIRMs) identify risk zones and often include Base Flood Elevations that affect building rules and insurance pricing. Zones A, AE, V, or VE are Special Flood Hazard Areas, which typically trigger lender-required flood insurance when you have a federally related mortgage. Zone X is lower risk and does not trigger the federal mandate, though insurance is still available. Learn the basics from FEMA’s overview of flood zones and SFHAs and the definition of Base Flood Elevation.

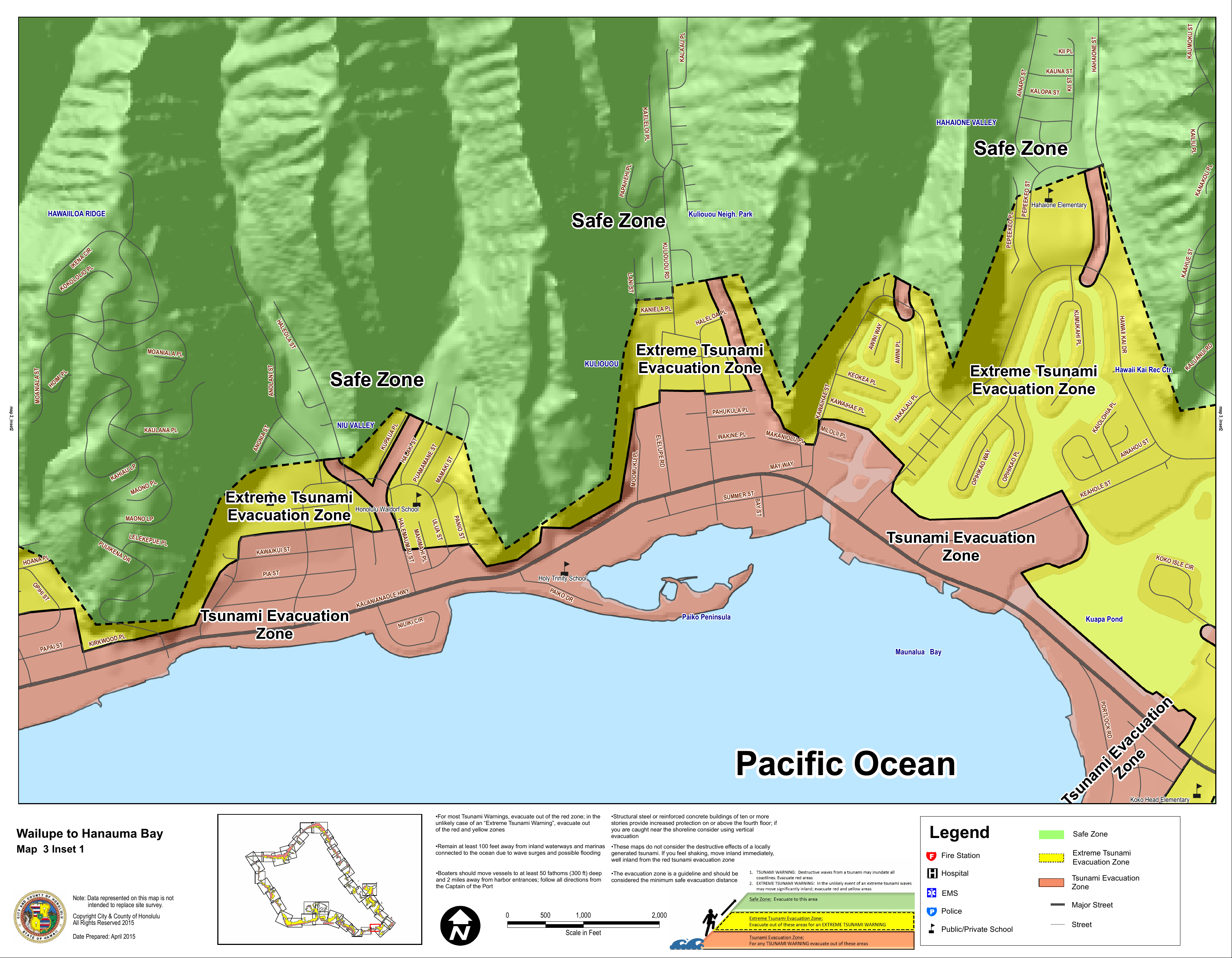

Tsunami maps and FEMA maps serve different purposes. A home can be inside a tsunami evacuation zone and not be in a FEMA Special Flood Hazard Area, or the reverse. In ʻĀina Haina, many makai frontage streets near Maunalua Bay appear inside the tsunami evacuation shading, while streets even a few blocks mauka sit outside those zones. See the shoreline detail in the Wailupe to Hanauma Bay inset for a neighborhood-level view. Use tsunami maps for life-safety planning and FEMA maps for insurance and permitting.

Use the FEMA Flood Map Service Center to look up the property by street address or TMK. You will see the current effective flood zone and any Letters of Map Change that affect the parcel. Start here for any insurance or lender question: FEMA’s Map Service Center.

Open the HI‑EMA tsunami page and pull the downloadable insets for the ʻĀina Haina and Wailupe shoreline. Confirm whether the parcel is shaded as a “Tsunami Evacuation Zone” or “Extreme Tsunami Evacuation Zone.” These maps guide where and how to evacuate during an event. Use the state’s tsunami resource hub.

Hawaii’s Flood Hazard Assessment Tool shows FEMA’s digital maps on a local base map and includes an estimated ground elevation feature. While FHAT is informational only, it is useful for quick triage and for discussions with your lender or insurer. Explore the DLNR FHAT tool.

If your mortgage is federally related and the home is inside an SFHA on the effective FEMA map, the lender must ensure you carry flood insurance. Servicers follow standard flood determination practices and will track compliance throughout the life of the loan. See FEMA’s guidance on lender determinations through the Map Service Center.

Standard homeowners insurance does not cover flood or tsunami inundation. The National Flood Insurance Program typically covers flood damage caused by tsunamis, subject to policy terms and limits. Standard NFIP limits for a single-family residence are commonly $250,000 for the building and $100,000 for contents. There is often a 30-day waiting period before a new policy becomes effective, so start early. Review FEMA’s tsunami and NFIP explainer in this official fact sheet.

Private flood insurance has expanded and can sometimes offer higher limits or different terms. Many lenders can accept qualifying private policies to meet the federal requirement, but acceptance depends on specific policy language and regulations. Ask your lender what documentation they need and compare quotes. For a regulatory overview, see this private flood insurance summary.

FEMA’s updated Oʻahu flood maps moved through the review process, with a Letter of Final Determination issued December 10, 2025, and an effective date scheduled for June 10, 2026. If a parcel is newly mapped into an SFHA, lenders may begin enforcing mandatory purchase around the effective date. Confirm which map panel your lender will use for your specific parcel and plan accordingly. Local update details are summarized in the state’s outreach on Oʻahu flood map changes.

Hawaii’s seller disclosure statute requires sellers to disclose if the property lies within a FEMA Special Flood Hazard Area, a tsunami inundation map, or a designated sea-level-rise exposure area. For shoreline properties, permitted or unpermitted erosion-control structures must also be disclosed. You should still verify independently. Read the statute summary for HRS 508D-15.

Ask the seller or listing agent for:

If needed, include contingencies that require these items within a set time frame. Neutral, factual wording keeps the focus on risk and documentation.

If the map shows the lot inside an SFHA but a certified survey shows the lowest ground or building elevation above the Base Flood Elevation, you may be able to request a Letter of Map Amendment or Revision. A successful LOMA can remove the federal insurance mandate for a federally related mortgage, though you may still choose to insure. The process is technical, and many buyers hire a licensed surveyor or engineer. Start with FEMA’s LOMC process guide.

Honolulu’s Department of Planning and Permitting flags flood status during permit intake. Properties in regulated flood zones may require additional documentation, including Elevation Certificates, engineered foundation details, flood vents, or floodproofing certifications. Work with a local design professional familiar with the city’s HNL Build portal to avoid delays. Read an overview of how flood layers can affect permits in this local permitting explainer.

Common measures include elevating the lowest habitable floor above the Base Flood Elevation, relocating utilities above the design flood elevation, using flood-resistant materials below BFE, and installing compliant foundation openings. In coastal high-hazard zones, avoid enclosed living space below the required elevation. Plan for longer review times and higher costs when flood documentation is required. For definitions that guide designs and ratings, revisit FEMA’s BFE glossary entry.

Buying in ʻĀina Haina should feel confident and clear. If you want local, step-by-step guidance on parcels mauka and makai of Kalanianaʻole Highway, connect with a neighborhood expert who can help you navigate maps, insurance, and negotiations so you can focus on island living. Reach out to Chelsey Flanagan to get started.

Stay up to date on the latest real estate trends.

From personalized search criteria, email updates for new or changed listings, community and school demographics, satellite map searches to free market reports, forms, and updated real estate news. Feel free to contact me and I will be happy to help you with all your real estate needs.

{kind=link}